MRTA vs MLTA

Securing Your Home: The MRTA vs. MLTA Dilemma

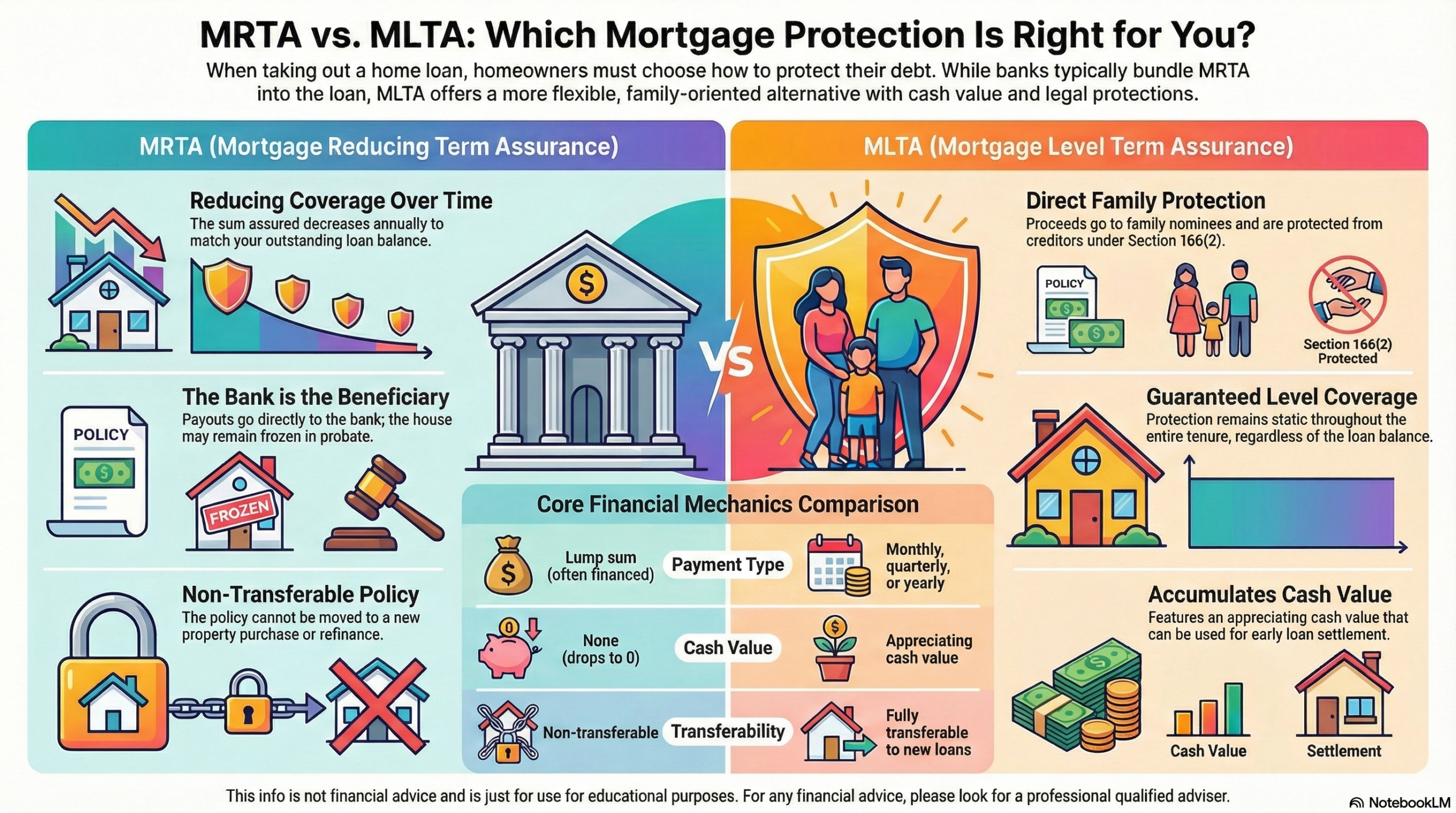

Deciding between MRTA (Mortgage Reducing Term Assurance) and MLTA (Mortgage Level Term Assurance) is a common hurdle for new homeowners. While both aim to provide protection, they function in fundamentally different ways that can impact your family’s financial future.

What is MRTA?

Mortgage Reducing Term Assurance (MRTA) is a life insurance plan where the sum assured decreases over time, specifically tailored to match your declining home loan balance. Bank officers often recommend it because it is a “hassle-free” one-time payment that can be financed into your mortgage loan.

However, the primary beneficiary of an MRTA is the bank. In the event of a misfortune, the insurance company pays the outstanding loan balance directly to the bank. While this clears the debt, your house may still be frozen under your estate. If your total liabilities exceed your assets, your family could be forced to walk away from the home despite the insurance payout.

What is MLTA?

Mortgage Level Term Assurance (MLTA) provides static or level protection throughout the entire tenure of your loan. Unlike MRTA, the beneficiary is your family (provided the policy is a trust policy).

A significant advantage of MLTA is that it is protected under Section 166(2) of the Insurance Act of Malaysia 1996. This legal safeguard ensures that the insurance proceeds are paid directly to your nominees and do not form part of your estate, meaning they cannot be seized by creditors to pay off other debts. Your family can then use this money to settle the house or even buy a new one.

Key Differences at a Glance

To help you choose, here are the major distinctions between the two:

-

Payment Structure: MRTA usually requires a lump sum payment upfront, often financed into the loan, which means you pay compounding interest on it. MLTA premiums are generally higher but can be divided into monthly, quarterly, or yearly payments without extra charges.

-

Cash Value: MRTA has a decreasing cash value that eventually drops to zero. In contrast, MLTA has appreciating cash value, which can potentially be used for early settlement of your loan.

-

Transferability: MRTA is tied to a specific loan and is non-transferable. MLTA is highly flexible; it can be attached to any loan and transferred if you purchase a new property or refinance.

-

Protection Level: MRTA coverage reduces annually as you pay off your loan. MLTA coverage remains constant, and if the payout is more than the remaining loan, your family keeps the difference.

Which Should You Choose?

If you prioritize a policy that protects your family directly, offers cash value, and remains flexible across different properties, MLTA is often considered the superior choice. While it may be slightly more expensive, the legal protections and the ability to use its cash value for debt cancellation offer long-term financial benefits that an MRTA cannot match.

Ultimately, the choice depends on your financial goals. If you have already decided on an MLTA, be sure to inform your bank officer that you have your own policy in place.

Alex Song, CFP® is the Principal of All Weather Portfolio PLT (awfp.my) and the founder of AdvisorX (advisorx.app), a Malaysia-based financial advisory firm focused on transforming how individuals and businesses approach financial planning in the digital age. As a Certified Financial Planner (CFP®) and an HRD Corp Certified Train-The-Trainer (TTT), Alex brings both technical expertise and strong educational impact into his work. He leads a unique three-pillar B2B2C business model that bridges financial education with actionable advisory solutions. Through this proven approach—combining corporate training, public financial education, and personalized advisory—Alex has guided countless clients toward achieving debt-free retirement and making smarter, more confident wealth decisions.

View All Articles