A Malaysian’s Winning Philosophy for Financial Freedom

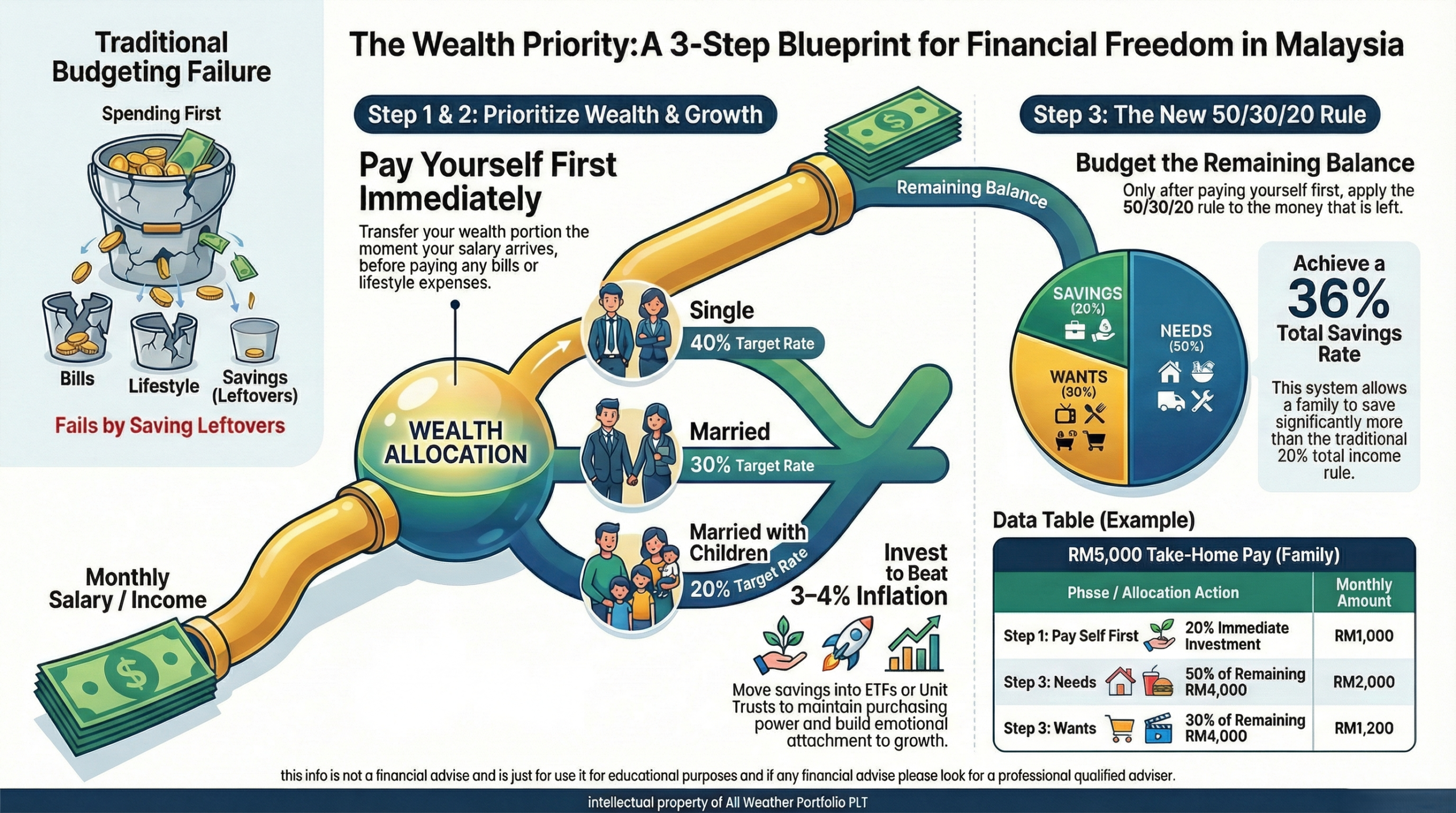

In Malaysia, the traditional budgeting rule of 50% Needs, 30% Wants, and 20% Savings is widely taught, but it often starts with the wrong focus: spending first and saving later. This approach frames your finances around the question, “How much can I spend?”.

To truly achieve financial freedom, you must flip this mindset and ask, “How much can I build?”. When savings come last, they are frequently reduced, delayed, skipped, or used as a backup for overspending. You do not grow wealthy by leftover money; you grow wealthy by intentional money.

Step 1: Pay Yourself First (Before Anything Else)

“Paying yourself first” means prioritizing your future wealth before you pay for your mortgage, car loan, food, or subscriptions. By transferring a set percentage of your income out the moment your salary hits your account, your lifestyle automatically adjusts to the remaining balance.

The amount you should set aside depends on your life stage:

Single: Save and invest 40% of take-home pay.

Married (no children): Save and invest 30%.

Married with children: Save and invest 20%.

This creates the discipline and momentum needed to reduce lifestyle inflation and build long-term wealth.

Step 2: Invest the Amount You Set Aside

In the Malaysian context, simply saving in a regular bank account or Fixed Deposit (FD) is insufficient because inflation (averaging 3–4% yearly) slowly erodes your purchasing power. You must put your money into growth assets like ETFs or Unit Trusts.

There are three key reasons why investing—rather than just saving—is critical for your winning philosophy:

It Builds Momentum: As your investments grow, that growth builds confidence, and confidence builds the consistency needed to stay on track.

It Creates Emotional Attachment: When you see a growing portfolio, you feel a sense of ownership that makes you hesitate to withdraw money unnecessarily. Savings accounts are too easy to withdraw from, and FD maturities often get spent.

You Can Use Profits Strategically: You can eventually sell your investment gains to fund a house renovation, a family holiday, or a lifestyle upgrade, all while keeping your principal working for you.

Investing feels like wealth building, and that psychological difference is what keeps you committed.

Step 3: Manage the Remaining Money Monthly

Once you have paid yourself and invested that portion, you budget the remaining balance. This is where the 50/30/20 rule becomes a useful reference framework:

50% Needs: (Rent, mortgage, utilities, transport).

30% Wants: (Dining, lifestyle, holidays).

20% Additional Buffer: (For unexpected costs).

Applying this to the leftover amount ensures your commitments stay manageable without ever sacrificing your wealth building. For example, a Malaysian earning RM5,000 (married with kids) who invests RM1,000 (20%) first and then budgets the rest can achieve a total savings rate of 36%.

Why This Works for Malaysians

This system is specifically designed to address common local financial hurdles, such as the “car loan culture” and a heavy reliance solely on EPF. In Malaysia, “car loan culture” refers to the tendency to prioritize high monthly car installments as a status symbol or necessity, often taking on long-term debt that eats away at potential savings before wealth is even built. By paying yourself first, you ensure that your future is secured before these car loans and other lifestyle commitments take over your paycheck.

Furthermore, it is important to realize that it is not how much you earn that determines your savings, but your financial structure. We often see:

• B40 individuals who exercise extreme discipline and manage to save 40% of their income.

• High-income earners who have nothing left to save because they are trapped by high-commitment lifestyles, overspending on credit cards, and multiple unsecured loans.

This philosophy works whether you earn RM3,000, RM5,000, or RM10,000 because it relies on behavioral structure rather than income level. It shifts you away from “leftover” thinking and toward a “priority” mindset.

Final Thought

Financial freedom is not about making more money, finding a “hot stock,” or timing the market. It is about consistent behavior over time.

My philosophy is simple:

Pay Yourself First

Invest the Rest

Budget Smart Monthly

Start building first, then enjoy later. Wealth is not built by leftovers; it’s built by priority.

Alex Song, CFP® is the Principal of All Weather Portfolio PLT (awfp.my) and the founder of AdvisorX (advisorx.app), a Malaysia-based financial advisory firm focused on transforming how individuals and businesses approach financial planning in the digital age. As a Certified Financial Planner (CFP®) and an HRD Corp Certified Train-The-Trainer (TTT), Alex brings both technical expertise and strong educational impact into his work. He leads a unique three-pillar B2B2C business model that bridges financial education with actionable advisory solutions. Through this proven approach—combining corporate training, public financial education, and personalized advisory—Alex has guided countless clients toward achieving debt-free retirement and making smarter, more confident wealth decisions.

View All Articles